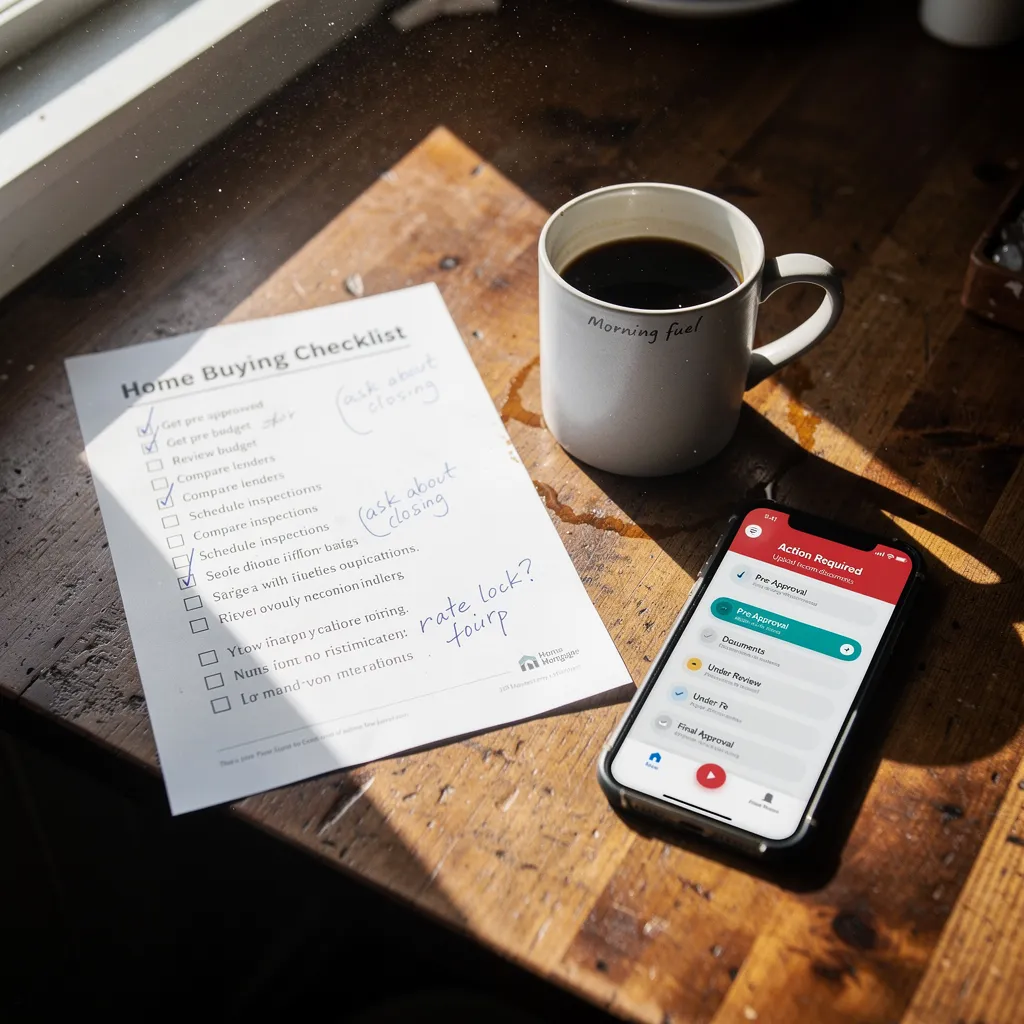

Home Buying Checklists for First Time Owners: here's what actually helps.

After you’ve made an offer on a home - you’ll need to select a loan offer by comparing lenders’ official offers, weighing your options, and choosing the best one for you. And once you’ve picked your mortgage loan, it’s time to prepare for closing by submitting paperwork and staying organized.

To help you through the process, here are some key things to remember.

Home Buying Checklists for First Time Owners

If you’re thinking of buying your first home - you might feel overwhelmed with all the information out there. But by breaking it down into a series of tasks, you can simplify the process.

The Consumer Financial Protection Bureau suggests starting by getting prepared to shop for homes, figuring out how much house you can afford, and learning what to expect during the buying process and when you apply for a mortgage.

Prepare to Shop for Homes

Once you’ve decided that you’re ready to buy a home, it’s time to get started. Here’s what you need to know:

Get a Preapproval Letter for Your Mortgage

A preapproval letter tells sellers you can get a mortgage for a certain amount at a certain interest rate. This can help you compete with other buyers and negotiate better terms with sellers.

To get preapproved - gather all your financial documents and fill out a mortgage application. You might also be able to apply online. Lenders typically require:

Some lenders might ask you for additional information, including a copy of your driver’s license, a recent pay stub, and copies of your credit report.

Learn What to Expect During the Buying Process

You’ll probably work closely with a real estate agent and a mortgage lender during the homebuying process. Here’s what you can expect from each:

Real Estate Agents

Your agent will help you find a home you like and that fits within your budget. He or she can provide information about a property, arrange showings - and help you negotiate a fair price. You’ll sign a contract with your agent before you start looking for a home.

The contract should specify what the agent will do for you, such as:

Mortgage Lenders

Before you apply for a mortgage, you should compare lenders’ products and services. You can do this by asking lenders questions, getting quotes, and comparing their offers. The Consumer Financial Protection Bureau suggests you compare:

You can also compare lenders based on:

Choose a Loan Offer by Getting Official Loan Offers from Lenders

Once you’ve made an offer on a home - you can start comparing lenders’ official loan offers. You can do this by:

Then, compare lenders’ offers based on the following criteria:

You can also consider other factors, such as the customer service you receive and the lender’s reputation for fairness and transparency.

Get Ready to Close by Submitting Paperwork and Keeping Track of Necessary Items

Once you’ve selected a mortgage loan, you’ll need to prepare for closing. Closing is when you finalize the purchase of your home. You’ll sign all the paperwork and pay closing costs. Closing usually happens in a lawyer’s office, but it can also happen electronically.

Here’s what you need to do before closing:

Submit Paperwork

Submit all the paperwork required by your lender. This might include:

You should also submit any other documentation required by your lender. For example - if you’re self-employed, you might need to submit business records.

Keep Track of Necessary Items

Keep track of any items you need to bring to closing. This might include:

You might also need to bring other items to closing. Ask your lender or real estate agent what else you need to bring.

FHA Loans

One option for financing your first home is an FHA loan. These loans are insured by the Federal Housing Administration (part of HUD) and have been helping people become homeowners since 1934. They're designed for low- to moderate-income borrowers who don’t have a lot of money saved up for a down payment.

FHA loans require a lower down payment than conventional loans, and they have less strict credit requirements. However, FHA loans come with higher monthly mortgage insurance premiums and a higher upfront mortgage insurance premium.

Before applying for an FHA loan, you should research the pros and cons of this type of loan. You can do this by talking to a lender - reading reviews, and using a website that compares FHA loans.

When you’re ready to apply for an FHA loan, gather all your financial documents and fill out an application. You can usually apply for an FHA loan online or in person. Once you’ve submitted your application, a lender will review it and let you know if you’re approved.

Conclusion

Buying a home for the first time can be overwhelming, but by breaking it down into steps - you can simplify the process. Start by preparing yourself to shop, figuring out how much house you can afford, and learning what to expect during the buying process and mortgage application. Then, choose a loan offer by comparing lenders’ official offers and selecting the best one for you. Finally, prepare for closing by submitting paperwork and keeping track of necessary items.

Remember - buying a home is a big decision, so take your time and do your research. With a little preparation, you can find the perfect home for you.